When you bought your first home, everything was pretty much perfect. You had the right amount of space, the location was convenient, and the house had the amenities you were looking for.

Fast-forward a few years, and your life has changed. You might have expanded your family, accepted a new job, or started longing for some upgrades. Your first home no longer seems like the ideal place to live. There’s not enough space, it’s too far from work, or it lacks the features you need.

While your first home may no longer meet your needs, it’s likely that it’ll meet the needs of someone else. You might be able to find a tenant who would be happy to call your house home.

Renting out your first home instead of selling it can provide several benefits. For one, as long as the property is rented, you’ll have an extra source of income. Depending on the market, there might be a considerable demand for rental properties, meaning you can likely charge market rates or higher per month.

Another benefit of renting out your first home after buying your second property is that it gives the property a greater chance to increase in value. It’s possible that the value of your home has fallen since you purchased it. If you try to sell the house and can’t get what you paid for it or what you still owe on the mortgage, there’s a chance you’ll have to pay out of pocket to make up the difference. Renting out your home instead of selling it gives you more time to watch the market and sell when it’s most financially beneficial for you.

The process of getting a second mortgage and buying a second home is similar to the process of buying your first home and getting your first mortgage, but there are a few fundamental differences, especially if you aren’t selling your first property. Learn more about what to expect when you want to rent out your home and buy another.

How to Get a Mortgage for a Second Home

When you’re applying for a mortgage to buy your second home, it’s important to understand that the mortgage you’re applying for is different from a second mortgage. A second mortgage typically refers to a home equity loan. It’s a loan against the house you currently own and have built up equity in. You generally can’t use the funds from a second mortgage to pay for an entirely different home, although you might be able to use some of the funds from a home equity loan for a down payment on your new mortgage.

It can be trickier to qualify for a mortgage on a second property, especially if you don’t plan on selling your current home and using the proceeds to pay down your first mortgage. One reason for that is the fact that you’ll continue to owe and make payments on the first home that you’re planning to rent out. While you may eventually be able to refinance in order to combine the two loans into one, that isn’t always the best move since your current interest rates may be lower than ones you could get when you refinance.

Before you start looking for your new home and shopping for a mortgage, it can be helpful to use a mortgage calculator to help you understand whether buying a second home without selling the first one is a viable option for you.

How much debt you currently have and your income aren’t the only things you want to pay attention to when you apply for an additional mortgage. You also want to be aware of your credit score, which could impact your eligibility to get a loan and the rate you’ll pay.

During this time, to keep your credit score high, continue making on-time payments on your existing mortgage. Avoid applying for new credit cards or other loans in the months before you apply for a new mortgage, too.

You’ll also want to save up a considerable amount to put toward the down payment, as well as the closing costs on the new mortgage. As with your first home, you’ll want to have an emergency fund to cover maintenance on the new home and any sudden, necessary repairs. Since you’ll own two properties, it’s smart to have enough of a cushion to pay for maintenance and repairs on both homes.

As we mentioned above, you might be able to use the funds from a home equity loan to cover the down payment on your second home. There are risks involved in doing so, though. You’re borrowing against one property to pay for another, which can put you at risk of losing both properties if you fall behind on payments.

Another consideration with using a home equity loan to fund a down payment is that the interest rate on home equity loans tend to be higher than the interest rates on a primary mortgage. Depending on the interest rates you qualify for, if you can afford the higher monthly payment, it might be less expensive to make a lower down payment rather than using money from your first home’s equity.

Getting Preapproved for a Mortgage

Once you’ve calculated the numbers and know you can comfortably afford two mortgages, if your credit is in good shape, it’s time to get preapproved for your new mortgage. A preapproval is like getting a stamp of approval from a lender. It means a lender has looked at your income documents, your existing debt, and your credit, and has determined that you are a qualified candidate for a home loan.

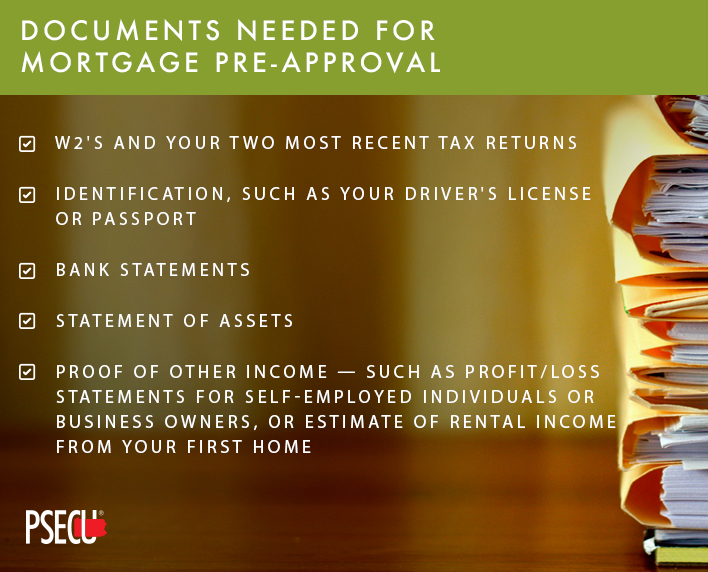

To get preapproved for a mortgage, you’ll usually need to present proof of income and savings. The types of documents you’ll need to provide may include (but are not limited to):

- W2’s and your two most recent tax returns

- Identification, such as your driver’s license or passport

- Bank statements

- Statement of assets

- Proof of other income — such as profit/loss statements for self-employed individuals or business owners, or estimate of rental income from your first home

Understand Your Mortgage Options

Although a preapproval letter can help to make you a more viable candidate when you’re looking for your second home, it’s not a guarantee that you’ll be able to get a mortgage when the time comes, nor does it lock you into a particular type of mortgage. It’s meant to be a baseline you can use during your search for a new home.

As when you bought your first home, you have a variety of different mortgage types to choose from when purchasing a second property. One thing to consider is the type of interest rate.

Fixed-rate mortgages charge the same interest rate over the entire term of the loan. If interest rates drop while you’re paying down the mortgage, you’ll need to refinance the loan to take advantage of lower rates. On the other hand, if rates increase, you can still enjoy a lower rate.

The interest rate on an adjustable-rate mortgage changes with the market. Your initial rate might be locked in for a certain time, such as three or seven years. After that, the rate will change, usually annually, based on the market. With an adjustable-rate mortgage, you might get a very low rate up front, only to have rates jump after a few years, increasing your monthly payment.

Mortgages also differ when it comes to the term, or how long you make payments on them. The rate charged on the loan often varies based on the term. Shorter term loans typically have lower rates than 20- or 30-year mortgages. If you’re buying a home in Pennsylvania, view our mortgage terms and interest rates here.

What to Consider When Renting Out Your First Home

Before you decide to rent out your home and buy a second home, it’s a good idea to make sure you understand the responsibilities and whether your current home will be a desirable place for renters to live. Here’s what to think about:

1. How Rentable Is Your First Home?

One of the first things to consider is how rentable your first home is. Ideally, there will be demand for your home from renters in the area, and it won’t languish on the market waiting for a tenant.

Not every home makes a good rental property. Some homes are just too big to appeal to the average renter, while others might be too small. Usually, a property with two or three bedrooms will have a broader appeal than a property with six bedrooms or just one bedroom.

The condition of your home can also determine how appealing it is to potential tenants. If a property needs a lot of work or generally looks rundown and worn out, it can be difficult to find tenants for it. No one wants to live in a house with a lot of issues. Plus, a property that shows signs of neglect can raise red flags for tenants, who might think that the landlord is going to be less than attentive to their needs.

2. What Is the Local Rental Market Like?

Another thing to pay attention to when deciding whether to rent out your first property is the state of your local rental market. Are rentals in demand where you live? Or do apartments sit vacant for months, waiting for someone to call them home?

It’s also a good idea to get an understanding of the amount of rent charged for properties like yours. Ideally, the monthly rent you charge will be higher than your monthly mortgage payment. Otherwise, it might be difficult for you to pay the mortgage on the rental and cover the costs of maintenance and upkeep.

3. Should You Hire a Property Management Company or Not?

You’ll also want to weigh the pros and cons of hiring a property management company for your rental property. If you’re entirely new to being a landlord, working with a property management company can help you get your feet wet and avoid some of the stressors associated with working with tenants.

For example, if a tenant doesn’t pay their rent, it’s the property management company who will follow up with them or start the eviction process, if warranted — not you. Property management companies can also handle tenant screening, showing the property to interested renters, and scheduling maintenance and repairs.

Working with a property management company can be particularly beneficial if you’re moving to an area that’s a far commute from your original home. It’s also helpful if you’ve got a lot on your plate.

That said, property management companies do come at a cost. You might have to increase the amount of rent you charge tenants to afford the added expense.

4. What Are the Rental Rules in Pennsylvania?

The rental rules, or landlord-tenant laws, tend to differ from state to state. Pennsylvania has its own set of landlord-tenant laws. If you’re going to rent out your home, it’s important that you know what your rights are as a landlord and what rights your tenants have.

PA landlord-tenant law also lays out the proper process for evicting tenants and explains when tenants have a right to withhold their rent. Knowing the laws will help keep both you and your tenants happy with the agreed-upon arrangements.

5. What Are the Taxes Associated with a Rental Property?

Renting your home out can change your tax situation. You’ll most likely need to report the income you get from the property as income on your tax return. In many cases, you’ll be able to deduct expenses associated with renting out your home on your tax return. It’s a good idea to work with a tax professional to make sure you are correctly reporting your rental income and expenses.

You’ll also want to think about real estate tax when you rent out your home. Some areas have a homestead exemption, which reduces the amount of property taxes owners who live in their properties pay. Once you move out of your first home and start renting it, you’ll most likely no longer qualify for that exemption, which may raise your taxes.

6. How Long Have You Lived in Your First Home?

One more thing to consider when buying a second home and renting out your first one is how long you’ve lived in your first property.

Mortgage terms and conditions for primary residences and rental properties tend to be different. A mortgage that’s specifically for a rental property often has higher interest rates and might require a larger down payment. If you got your first mortgage for a primary residence, you might be expected to remain in the house as a resident for a specific amount of time, such as one or two years. After that period, you’ll be able to move out and rent it. But trying to rent out your home before the residency period is up can have consequences.

The Financial Picture: Can You Afford to Be a Landlord?

Some people look at being a landlord as a quick and easy way to make money. The reality is a bit different, though. It can often cost a lot more than expected to be a landlord, and the money, in the form of rental income, might not come pouring in.

One essential question to ask yourself when deciding whether you can realistically afford to be a landlord is: Can you cover the cost of both mortgages if you don’t have someone living in your property paying rent? If the answer is no, or it would be a challenge, then renting out your first property might not be the right option for you at the moment. You don’t want to run the risk of missing payments on one or both of your mortgages.

Another question to ask to determine whether you can afford to be a landlord is: Can you afford to make repairs to the property as needed?

When it’s your own home, you can usually get by without certain things for a while. If your air conditioning unit breaks and you don’t have the funds to repair it, you might be fine putting up with the heat until you have the money to repair the existing unit.

With a tenant, it’s a different story. If something breaks in a rental property that makes it uninhabitable or otherwise not up to snuff, you need to fix it as soon as possible.

Ideally, you’ll have some money in savings earmarked for repairs to your rental property. If you don’t have that, another option is to have access to credit, such as credit card or home equity line of credit, so that you can cover the cost of necessary repairs right away.

Other costs associated with being a landlord include marketing the property between tenants and performing general updates to reduce signs of wear and tear. Both can add to the cost of being a landlord, so it’s important to make sure you have room in your budget to cover them.

There are also worst-case scenarios to consider. While you might get lucky and find good tenants right away, there’s also a chance you’ll get saddled with tenants who could be difficult to deal with. Destroyed property and late rent payments could cost you a considerable amount of time and money, in the form of extensive repair costs or legal fees.

Additionally, you’ll want to consult with your insurance agent to determine how changing your home from your primary residence to a rental property can impact your rates.

When you’re estimating how much it’ll cost to be a landlord, it’s better to overestimate your expenses. Calculate the cost of your mortgage, property taxes, property management fees, insurance, and estimated repair costs, as well as any additional expenses you anticipate when renting your home. If what you can charge in rent meets or exceeds that amount, still leaving you with a cushion you’re comfortable with each month, and you have a few months of estimated expenses in reserve, then becoming a landlord may be something you can afford to take on.

Are you ready to start looking for your second home? We can help. We offer competitive interest rates and a variety of payment terms to meet your needs and your budget. Learn more about our mortgage options and get in touch today to get started on the path to renting out your current home and moving into your next one.