There are a lot of reasons why you might switch jobs. Your current job might be “just to pay the bills,” and you might have found an opportunity to pursue a career that aligns with your interests. You might have to move because your partner got a new gig or because you want to be closer to your family. You may have found a higher paying role at a new company, or you might be switching to a fast-growing industry, hoping to give yourself more opportunities for advancement.

Whatever your reasons for wanting a new job, there are some financial considerations to think about before you leap. A new job might come with a salary increase, but depending on the benefits package and other factors, it might not be as financially beneficial as your current position.

Whether you have an offer in hand or are just beginning to think about making a career change, here’s what to consider before you make a move.

1. Time Between Paychecks

In a perfect world, you’d wrap up at your current job, start your next one, and have no time in between paychecks. In reality, there might be a gap between pay periods when you switch careers.

If you’re a contractor, one contract might end several weeks or months before the next one begins. If you’re a teacher, you might get your last paycheck from your old school at the end of the school year. You might have a job lined up for the fall, but you’ll have to wait until then to start collecting your salary.

It might also be the case that you’ve decided to take some time off between jobs. You might leave your current situation with another position lined up. But instead of starting your new role immediately, you might choose to take a few weeks or even a month off between positions, giving yourself time to travel or work on a few projects around the house.

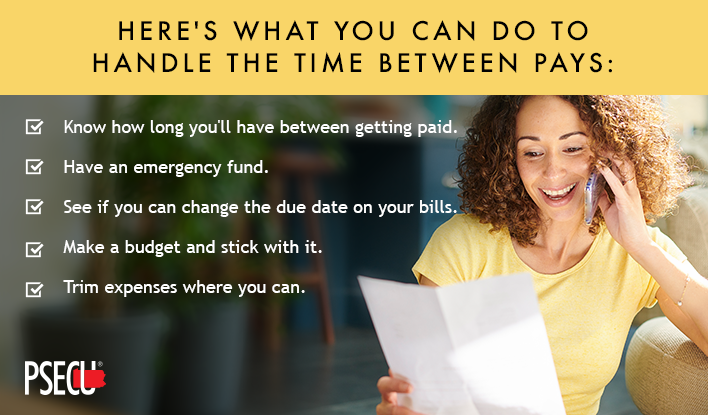

No matter the reason for the gap in pay, it’s something to plan for when you’re changing jobs. Here’s what you can do to handle the time between pays and help keep your finances afloat while you wait to start your new position.

- Know how long you’ll have between getting paid. You not only want to know when to expect your last paycheck from your former employer, but also when you can expect your first paycheck from your new job.

- Have an emergency fund. Before making the switch, it’s a good idea to have some money set aside to act as a cushion and to cover your living expenses until you get paid by your new employer. How much you’ll need depends on your current cost of living.

- See if you can change the due date on your bills. If you’re not moving for your new job, you might be able to ask your utility providers to change the date your bills are due. That way, you can align the due dates with your new pay schedule. Changing the due dates can also give you some wiggle room if there will be a week or two between paychecks.

- Make a budget and stick with it. Budgeting becomes particularly important during times of transition in your life, as it helps you understand what your obligations are and how much money you have available.

- Trim expenses where you can. Along with creating a budget, you might find that you need to cut back on your costs while you wait to get paid. Decide what you need and what you can live without. For example, you might pack your lunch for the first few weeks on the job to minimize the cost of dining out. You might also hold off on getting new work clothes until you get your first paycheck, provided you can make your existing wardrobe work.

2. Benefits Package

If your new job pays a lot more than your current one, it can look like a sweet deal, at least at first glance. But it’s a good idea to look beyond your base salary when you’re thinking about changing jobs. Benefits such as tuition reimbursement and paid time off paired with a lower salary may actually end up being more monetarily appealing.

Tuition Reimbursement

Some employers will reimburse you if you take classes at a college or university. Often, the courses you take need to be approved by your employer to qualify for the reimbursement. For example, if you’re an engineer, your employer might reimburse you if you enroll in a master’s or doctoral program in engineering. However, your employer is less likely to cover the cost of you taking theater or biology courses.

It’s also occasionally the case that an employer will cover the cost of your children’s college education. Universities and colleges often let the children of their employees attend for free or at a significantly reduced price. Some universities will even pay a portion of a child’s education costs at another school.

Paid Time Off

When you’re looking at job offers, take a close look at the paid time off the employer provides. If one employer lets you take 21 days per year, and another only offers 10 days, you might prefer the company that offers 21 days. The additional paid time off isn’t just a better deal for you. It also lets you enjoy a better work-life balance.

Paid Leave

If you need to take time off because of illness or because you’ve given birth to or adopted a child, the Family and Medical Leave Act allows you to take 12 weeks off during one 12-month period. Although you can take that time off if you need it, you’re not required to be paid during it.

That said, some employers do offer paid medical or maternity leave. If you have a medical condition that you know will require time off, are a caretaker for an ill family member, or are planning to grow your family, it’s worth it to understand the company’s policy regarding leaves of absence and whether you’ll be paid for them or not.

Health Insurance

For a lot of people, health insurance is the ultimate benefit. Although having an insurance plan through your employer can lower the cost of your premiums considerably, there’s a lot of variation when it comes to how much you’ll end up paying in premiums.

When choosing a plan, carefully look at the premiums, copays, and coverage offered. A lower premium might mean higher out-of-pocket expenses. Meanwhile, a higher premium might seem more expensive, but it can help you save on out-of-pocket healthcare costs. What’s best for you will depend on your personal situation and the health conditions of you and/or any dependents you’ll carry on your plan.

Profit Sharing

Another benefit an employer might offer is profit sharing. With profit sharing, you can earn shares or stocks in the company. Profit sharing plans are usually a type of retirement benefit. But instead of you contributing to the plan, your employer contributes for you by giving you company shares or cash. Like other retirement plans, you can use the money from profit sharing to help pay for your expenses once you’ve reached age 59-1/2.

Retirement Benefits

Instead of or along with a profit-sharing plan, your new employer might offer another type of retirement option, such as a 401(k) or 403(b). When comparing the retirement options from your new employer to your current retirement options, it’s essential to consider the following.

- Employer match. Some companies match the contributions their employees make to a 401(k) or similar plans. If your current employer offers a match and your new one doesn’t, you might end up earning less over the long term in your new job.

- Vesting. All of the money you contribute to a retirement plan is yours, no matter when you change jobs. If your employer matches your contributions, you may need to work for a company for a certain amount of time before their contributions become vested, meaning you own them. If you leave before you’re fully vested in the plan, you can lose the employer match.

- Rollover options. When you change jobs, you can sometimes leave your retirement plan alone. Another option is to roll it over into your new retirement plan or an IRA. Some plans require you to roll over the amount when you leave a job. If you do roll over the plan, it’s important to make sure you follow the guidelines associated with the plan. Otherwise, you might end up paying an early withdrawal penalty tax. Before making any decisions, speak with a trusted financial advisor to help understand how changing jobs could impact your retirement savings.

3. Cost of Living Increase or Decrease

When is $70,000 not $70,000? When you live in an area with a high cost of living. A $70,000 salary in an expensive city like New York won’t go as far as a $70,000 salary in Harrisburg, PA or Philadelphia, PA. If you’re currently making $70,000 and move to a pricier area for a job with the same salary, you’re essentially taking a pay cut, as your costs will go up, but your salary is staying the same.

On the other side of things, if you currently live in an expensive city and find a job with a similar salary in a less expensive area, you’re likely to see that your money goes much further. You might be able to set and achieve more financial goals with your new position and in a new location than you would if you stayed in an expensive part of the country.

4. Relocation Costs

Another thing to consider is the cost of moving for your new job. Whether you’re a do-it-yourself kind of person or hire a team of professionals to handle your move, relocating can be pricey.

Some employers will reimburse new hires for moving expenses. If a potential employer hasn’t mentioned covering relocation costs, it can be worth asking if they offer reimbursement.

If an employer is willing to reimburse you, find out if there’s a limit and what services the company will pay for. Some companies will pay for movers and packers, but they won’t pay for storage or for you to stay in a hotel between apartments or houses. Some will cover up to a certain amount, such as $5,000, which you can use for any moving-related costs.

Another thing to think about if you’re moving for your new job is the cost of leaving your social circle and family. How will you stay in touch once you’re in your new city? Will you have to travel back frequently to visit people? Of course, you might also be moving to be closer to your family or friends. In that case, you’ll end up saving on travel expenses in the long run.

5. Salary Negotiations at Your Current Job

If you like your current job, but it’s not paying the bills or if your salary is holding you back from reaching your financial goals, then it might be worth it to see if you can negotiate a higher salary from your current employer. Asking your boss for a raise can seem intimidating or challenging, but it might work out for you in the end. If you get to stay at a job you like and get more money out of the process, then you can consider that a win-win.

In some cases, it might not be that you need a higher salary. You might want to get other benefits from your current employer. Instead of asking for a raise, you might ask for more flexibility. For example, if you like your job, but the commute is a killer, you might ask if you can telecommute one or more days per week.

If the benefits at your current job leave something to be desired, see if your company is willing to work with you. You might ask if you can get a better 401(k) match or ask for additional paid time off.

If you do decide to use a job offer from another employer to open the door to negotiations with your current company, it’s a good idea to be cautious. If you want to stay at your job, you don’t want to run the risk of damaging your relationship. Be polite and courteous when asking for a raise and when mentioning the other offer from the competing company.

It’s also a good idea to be ready to accept the other job offer, in case your employer can’t boost your salary or offer you better benefits.

6. Growth and Advancement Opportunities

Although money matters when you’re choosing between jobs or in the process of changing jobs, it’s not the only thing to consider. You also want to think about the future opportunities available and how much room for growth and development each job offers.

For example, if you’re a professor at a small university, you might have advanced as far as you can at your current institution. Smaller schools often don’t have the funding or resources that larger institutions do. If you get a job offer from a larger research university, you’re likely to see an increase in salary and benefits, as well as more opportunities for career advancement. You have access to more research funding, a larger student talent pool, more colleagues, and more equipment and other resources. If you’re hoping to grow in your career and your field, taking the job with the larger school might make sense.

It might also be the case that your current job has plenty of growth opportunities, but you haven’t yet taken advantage of them or found out what they are. Before you start looking for a new job, it can be a good idea to sit down with your manager or supervisor and discuss your career path. Some of the questions you might ask include the following.

- Do you promote from within?

- What can I do to make myself a viable candidate for promotion?

- How long do people typically work here?

- Are there specific areas where you would like the company to grow?

Although many employers are happy to help their team grow and want to do what they can to retain top talent, not all do. If your current employer can’t answer your questions or seems hesitant to discuss your future with the company, it might be time to move on.

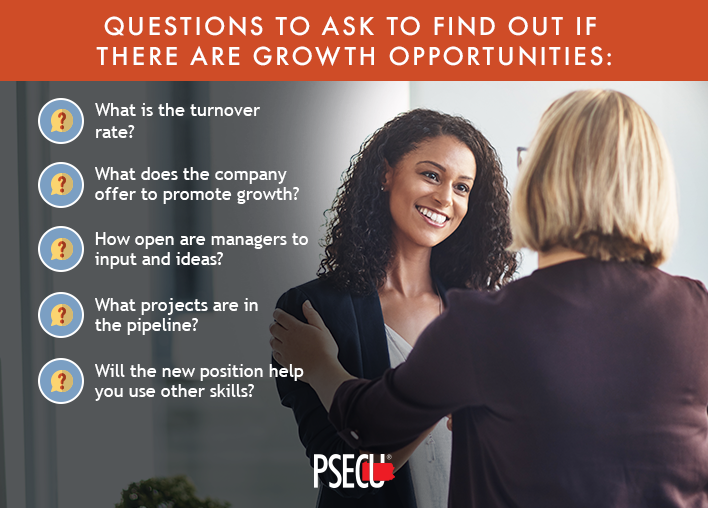

When you’re considering a new job, here are some of the questions to ask to find out if there are growth opportunities.

- What is the turnover rate? Do people stay with the company and move up? Or is it a revolving door of employees?

- What does the company offer to promote growth? Does it pay for continuing education or other training programs? Does it provide in-house programs to help you become better at what you do?

- How open are managers to input and ideas? Does your new manager seem open to ideas? Do they encourage you to share your thoughts and opinions on what the company can do to improve, or do they seem closed off to anything but the status quo?

- What projects are in the pipeline? What does the company have on the agenda for the next few months or years? How does it measure its results after each project?

- Will the new position help you use other skills? When you start your new job, will you be able to tap into skills that might be underused or not used at all in your current position? Will you have the chance to make use of a skill that you recently picked up in a class or seminar?

Set Savings Goals as You Advance in Your Career

A new job or career can be the next step forward in your life, allowing you to earn more and achieve more of your financial goals. As you get started on your next path, it’s a good time to reevaluate your financial institution’s products and services. If you’re looking to make a change to a financial institution that offers low- or no-fee products and services, consider PSECU. We offer IRAs for retirement savings, personal savings accounts, and checking accounts. Or, if you’re looking for tips on how to better manage your finances moving forward, our WalletWorks page is also full of information to help guide you through every stage of your financial life.